1. Contemporary Management Techniques

3. Activity-Based Costing and Management

4. Target Costing

5. Cost-Volume-Profit Analysis

6. Decision Making with Relevant Costs and Strategic Analysis

7. Job Costing

8. Process Costing

9. Cost Allocation

10. Standard Costing

11. Balanced Scorecard

Section 1: Contemporary management techniques:

Benchmarking: A process by which a firm identifies its critical success factors, studies the best practices of other firms or other units within a firm for achieving these critical success factors, and then implements improvements in the firm's processes to match or beat the performance of those competitors. (E. Blocher, K. Chen, & T. Lin, 2002)

Total Quality Management (TQM): A technique by which management develops policies and practices to ensure that the firm's products and services exceed customers' expectations by increasing product functionality, reliability, durability, and serviceability.

Continuous Improvement (kaizen): Managers and workers commit to a program of continuous improvement in quality and other critical success factors.

Activity-Based-Costing (ABC): A costing method which analyzes all activities within the production of a product. It is used to improve the accuracy of cost analysis by improving the tracing of costs to products or to individual customers.

Reengineering is a process for creating competitive advantage in which the company reorganizes its operating and management functions, often with the result that functions are modified, combined, or eliminated.

Theory of Constraint (TOC) is a strategic technique to help firms effectively improve the rate at which raw materials are converted to finished goods. TOC helps identify and eliminate bottlenecks.

Target Costing: product cost is determine on the basis of a given competitive price and a desired profit. In other words, a company determined the price and a desired profit level before determined the product cost.

Section 2: Basic Costing Concepts

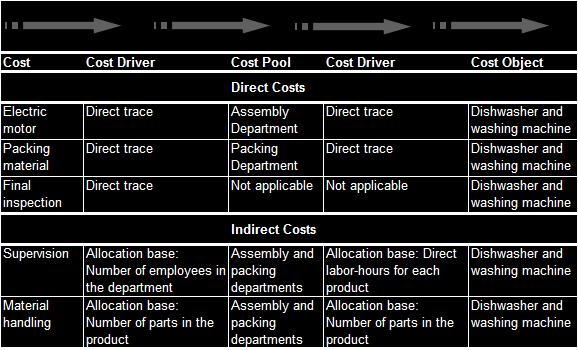

A. COST DRIVERS, COST POOLS, AND COST OBJECTS

A cost driver is any factor that has the effect of changing the level of total cost. A company incurs a cost when it uses a resource for some purpose. Costs are collected into meaningful groups called cost pools.

A cost object is any product, service, customer, activity, or organizational unit in which costs are assigned for some management purpose. Any item to which costs can be traced and that has a key role in management strategy can be considered a cost object.

A direct cost can be conveniently and economically traced directly to a cost pool or a cost object. In contract, an indirect cost cannot be conveniently and economically traced to a cost pool or a cost object.

Example of

Costs, Cost Pools, Cost Objects, and Cost Drivers in Appliance Manufacturing.

(Figure is taken from "Cost Management" 2nd Edition, Blocher, Chen, Lin.)

| Management Skills |

| Cost Management |

| Quantitative Analysis |

| Books Recommendation |

| Quotations |

| Stress Relievers |

| Home |

| Resume |

| About Me |